E-TAILING

E-tailing is the short-form for electronic retailing, tends to primarily focus on the business-to-consumer (B2C) and include Business-to -business, revolutionized the retail landscape by enabling businesses to sell products and services directly to consumers through digital platforms.

It leverages the internet to create a seamless shopping experience, allowing customers to browse, purchase, and often receive goods or services without physically visiting a store.

E-tailing ranges from large online marketplaces to individual company websites, offering convenience, a wide range of products, and the flexibility of 24/7 shopping. This innovation has transformed traditional retail, shaping consumer habits and business strategies in the digital age.

What are the products:

E-tailing offers a vast array of products across various categories. Some common products available in e-tailing include:

- Consumer Electronics: Such as smartphones, laptops, cameras, and accessories.

- Clothing and Fashion: Including apparel, footwear, and accessories.

- Home and Kitchen Appliances: Like refrigerators, microwaves, and vacuum cleaners.

- Books and Media: Including e-books, physical books, music, and movies.

- Health and Beauty Products: Such as skincare, makeup, and wellness items.

- Toys and Games: Including board games, video games, and educational toys.

- Furniture and Home Decor: Like sofas, tables, and decorative items.

- Groceries and Daily Essentials: Often available through online marketplaces or specific grocery e-tailers.

These are just a few examples, but the range of products available in e-tailing is continuously expanding, catering to diverse consumer needs and preferences.

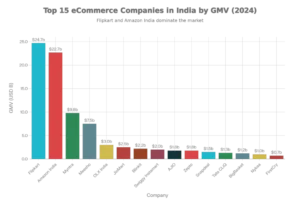

India E-commerce Market, by region : East India, West India, North India, South India

India E-commerce Kay Players are :

https://www.goodseva.com/blog/top-15-ecommerce-companies-india/

Response to E-tailing:

Customer response to e-tailing has been largely positive. It offers convenience, a wide array of products, and the flexibility to shop anytime and anywhere.

However, there are a few key aspects of customer response to e-tailing:

- Convenience: Customers appreciate the ease of shopping from their homes or on the go, eliminating the need to visit physical stores.

- Product Variety: E-tailing offers a vast range of products and services that might not be easily available in local stores.

- Price Comparison: Customers can easily compare prices across different platforms, allowing for more informed purchasing decisions.

- Customer Service: Prompt and efficient customer service can significantly impact customer satisfaction in e-tailing.

- Trust and Security: Concerns about online security and trust in the seller are factors influencing customer behaviour in e-tailing.

Overall, while e-tailing provides convenience and accessibility, ensuring security, trust, and excellent customer service remains crucial for fostering a positive customer response.

Payment Processing Options: –

Payment options in e-tailing are diverse, providing customers with various ways to complete transactions.

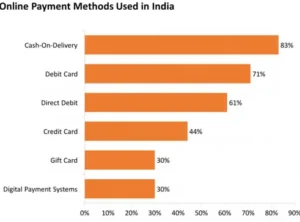

Online payment Methods Used in India in 2016

Common payment methods include:

- Credit/Debit Cards: The most used method, allowing customers to make payments directly from their cards.

- Digital Wallets: Such as PayPal, Apple Pay, Google Pay, and other similar platforms, enabling users to store payment information securely.

- Bank Transfers: Direct transfer of funds from the customer’s bank account to the seller’s account.

- Buy Now Pay Later (BNPL) Services: Offering the flexibility to make purchases and pay in instalments.

- Cryptocurrencies: Some e-tailers accept cryptocurrencies like Bitcoin as a form of payment.

- Mobile Payment Apps: Mobile-specific apps like Venmo, Cash App, or Alipay that facilitate transactions through smartphones.

- Cash on Delivery

These options provide flexibility and cater to different customer preferences, ensuring a smoother and more convenient purchasing experience in the e-tailing space.

Progress of online payments in India.

Online payments in India were on the rise, driven by factors such as increasing internet penetration, digital literacy, and government initiatives like demonetization. Popular methods included UPI (Unified Payments Interface), mobile wallets, and online banking.

Payment options in Brief:

1. Credit/Debit Cards:

Credit and debit cards are widely used in e-tailing for online transactions. They offer a convenient and secure payment method, allowing customers to make purchases without the need for physical currency. This helps streamline the checkout process, enhancing the overall user experience in e-commerce platforms. Additionally, credit cards often provide buyers with certain protections, such as chargeback options, in case of issues with the purchased items. Debit cards, on the other hand, deduct funds directly from the user’s bank account, offering a straightforward way to manage expenses in real-time. Overall, the integration of credit and debit card payments has become integral to the success of e-tailers in facilitating seamless and efficient online shopping experiences.

Certainly, here are examples of both credit and debit cards:

Credit Cards:

- Visa Credit Card: One of the most widely accepted credit cards globally.

- MasterCard: Another major credit card network with global acceptance.

- American Express (Amex): Known for its premium and rewards-oriented credit cards.

- Discover Card: Offers various credit card options with cashback rewards.

- Chase Sapphire Preferred: Known for its travel rewards and premium benefits.

- Citi Double Cash Card: Offers cash back on purchases.

- Capital One Venture Rewards Credit Card: Popular for travel rewards.

- Wells Fargo Cash Wise Visa Card: Known for its cashback rewards and simplicity.

Debit Cards:

- Visa Debit Card: Linked to a bank account, widely accepted for purchases.

- Mastercard Debit Card: Similar to Visa, linked to a bank account for transactions.

- Maestro: A debit card service provided by Mastercard.

- American Express Serve: A prepaid debit card option.

- Discover Debit Card: Linked to a checking account, often issued by banks.

- Chase Debit Card: Issued by Chase Bank for account holders.

- Citi Debit Card: Linked to a Citibank checking account.

- Bank of America Debit Card: Issued to account holders by Bank of America.

These are just a few examples, and there are many other credit and debit card options issued by various banks and financial institutions, each with its own features, rewards, and benefits.

Advantages of Debit and Credit Cards:

- Convenience: Debit and credit cards offer a convenient payment method for online transactions, eliminating the need for physical cash and simplifying the checkout process.

- Global Accessibility: Cards enable customers to make purchases from anywhere in the world, expanding the reach of e-tailers to a global audience.

- Security Features: Credit and debit cards often come with security features such as encryption, PINs, and authentication codes, providing a secure way for customers to make online payments.

- Fraud Protection: Many credit cards offer fraud protection, limiting the liability of the cardholder in case of unauthorized transactions, providing an added layer of security for online shoppers.

- Record-Keeping: Debit and credit card statements offer a detailed record of transactions, helping users track their expenses and facilitating budget management.

- Rewards and Incentives: Credit cards often come with rewards programs, cashback, or other incentives, giving customers additional benefits for using cards for their e-tail purchases.

- Instant Transaction Confirmation: Using cards provides instant confirmation of transactions, allowing customers to receive immediate feedback on their purchases.

- Easier Refunds and Returns: The use of cards simplifies the process of refunds and returns, as the funds can be credited back to the card, offering a smoother experience for both customers and e-tailers.

- Builds Credit History: Responsible use of credit cards can contribute to building a positive credit history.

Disadvantages of Debit and Credit Cards:

- Security Concerns: While cards come with security features, they are still susceptible to fraud, identity theft, and online security breaches, posing risks to the sensitive information of cardholders.

- Transaction Fees: Some e-tailers ma y charge additional transaction fees for using credit cards, impacting the overall cost for customers.

- Dependency on Technology: Electronic transactions depend on technology, and technical issues such as server outages or payment gateway failures can disrupt the payment process for both customers and e-tailers.

- Over-Reliance on Credit: The ease of credit card use can lead to overspending, accumulating debt, and potentially impacting the financial well-being of individuals who may not manage their credit responsibly.

- Exposure to Interest Rates: Credit card users may incur high-interest rates if they carry a balance from month to month, adding to the overall cost of their purchases.

- Limited Accessibility for Some Customers: Not all customers have access to debit or credit cards, especially in regions with limited banking infrastructure or for individuals who prefer alternative payment methods.

- Privacy Concerns: The use of cards involves sharing personal and financial information, raising concerns about privacy and the potential misuse of customer data.

- Chargeback Abuse: Some customers may abuse the chargeback system, leading to disputes and potential losses for e-tailers, especially in cases of fraudulent claims.

- Potential for Overshooting Credit Limits: Credit card users may unintentionally exceed their credit limits, leading to additional fees and negatively impacting their credit score.

- Incompatibility with Cash Transactions: In regions where cash transactions are still prevalent, the reliance on cards may limit accessibility for certain customers who prefer or rely on cash payments.

Despite these disadvantages, many measures, such as improved security protocols and user education, are in place to mitigate these risks. Users should stay vigilant and adopt secure practices when using debit and credit cards for online transactions.

2. Digital Wallets:

Digital wallets, also known as e-wallets, have become increasingly popular in e-tailing due to their convenience and security features.

Some Examples of Digital Wallets are:

- Apple Pay: Allows users to make payments using their Apple devices.

- Google Pay: Google’s digital wallet for making payments on Android devices.

- Samsung Pay: Samsung’s mobile payment and digital wallet service.

- PayPal: An online payment platform that also offers a digital wallet.

- Venmo: A mobile payment service that allows users to transfer money to others.

- Cash App: Enables users to send and receive money, as well as make purchases with a linked debit card.

- Square Wallet: A digital wallet service offered by Square, primarily focused on in-person transactions.

- Alipay: A popular digital wallet in China, offering various financial services.

- WeChat Pay: Integrated into the WeChat app, it’s a widely used digital wallet in China.

- Revolute: A fintech app that includes a digital wallet for international money transfers and spending.

These digital wallets provide convenient and secure ways to manage and use money digitally.

Advantages & characteristics of using digital wallets in e-commerce:

- Convenience: Digital wallets streamline the checkout process, allowing users to make quick and hassle-free transactions without entering extensive payment details for each purchase.

- Faster Transactions: Digital wallets often enable faster transactions compared to traditional payment methods, enhancing the overall speed of the online shopping experience.

- Security: E-wallets use encryption and tokenization to secure sensitive information, reducing the risk of fraud and unauthorized access to personal and financial data.

- Multiple Payment Options: Digital wallets can store various payment methods, including credit cards, debit cards, and bank account information, providing users with flexibility in choosing how to fund their transactions.

- Mobile Accessibility: Many digital wallets are accessible via mobile devices, allowing users to make purchases using smartphones or tablets, which is especially convenient for on-the-go shopping.

- Rewards and Cashback: Some digital wallets offer rewards programs or cashback incentives, providing users with additional benefits for using the wallet for their e-tail transactions.

- Integration with Loyalty Programs: Digital wallets can integrate with loyalty programs, allowing users to earn and redeem rewards seamlessly during their online shopping activities.

- Reduced Checkout Friction: With stored payment information, users experience reduced friction during the checkout process, leading to a more straightforward and enjoyable shopping experience.

- Offline Payments: Many digital wallets can be used for in-store purchases as well, providing a versatile payment solution that spans both online and physical retail environments.

- Trackable Transactions: Users can easily track their transaction history within the digital wallet, offering a convenient way to manage expenses and review past purchases.

Despite these advantages, it’s essential to consider factors such as compatibility with various e-tail platforms, user adoption rates, and regional preferences when assessing the integration and use of digital wallets in e-tailing.

Disadvantages of Digital Wallets in E-tailing:

While digital wallets offer various benefits, there are also some disadvantages in the context of e-tailing:

- Limited Acceptance: Not all online retailers or e-commerce platforms accept every type of digital wallet. This limitation can restrict consumer choice and convenience.

- Security Concerns: While digital wallets are designed with security features, there is always a risk of data breaches or hacking, potentially compromising users’ sensitive information.

- Dependency on Technology: Digital wallets rely on technology and internet connectivity. Technical issues, outages, or poor network conditions can hinder the user’s ability to make transactions.

- Privacy Concerns: Users may have concerns about the privacy of their personal and financial information when using digital wallets. Understanding how data is handled and secured is crucial.

- Compatibility Issues: Some digital wallets may not be compatible with certain devices or operating systems, limiting accessibility for users who prefer or are restricted to specific platforms.

- Learning Curve: Older or less tech-savvy users may find it challenging to adapt to using digital wallets, leading to a potential barrier for a portion of the consumer base.

- Transaction Fees: While many digital wallet services are free, some may charge fees for certain transactions or services. Users need to be aware of these potential costs.

- Loss of Device Concerns: If a user loses their device or it gets stolen, there is a risk that unauthorized individuals could access the digital wallet and make unauthorized transactions.

- Regulatory Changes: The regulatory landscape for digital wallets is evolving. Changes in regulations or government policies could impact how digital wallets operate and the level of consumer protection they offer.

- Dependence on External Factors: Digital wallets may be affected by changes in the financial industry, regulatory environment, or the companies providing these services. Users might be vulnerable to disruptions caused by such external factors.

Considering both the advantages and disadvantages, users and businesses need to weigh their priorities and preferences when deciding whether to adopt digital wallets in e-tailing.

3. Bank Transfers:

Direct transfer of funds from the customer’s bank account to the seller’s account. Bank transfers in e-tailing, or online retailing, are a common payment method. Customers can use electronic funds transfer to pay for products or services directly from their bank accounts. It’s a secure option, but some customers prefer more instant methods like credit cards or digital wallets for faster transactions.

Examples of Bank Transfer:

In the context of e-tailing (online retailing), bank transfers are typically used for certain payment methods. Here are some examples:

- Bank Transfer/Wire Transfer: Some online retailers provide the option for customers to pay by directly transferring funds from their bank account to the retailer’s bank account. This method is often used for large transactions or international purchases.

- Direct Debit: In certain regions, direct debit allows customers to authorize the retailer to debit the purchase amount directly from their bank account. This is commonly used for subscription services or recurring payments.

- ACH (Automated Clearing House) Payments: In the United States, ACH payments enable customers to make electronic transfers directly from their bank accounts to the retailer’s account. This is often used for online bill payments and purchases.

- Online Banking Payments: Some e-tailers provide an option for customers to pay directly using their online banking credentials. The customer is redirected to their bank’s online portal to complete the transaction.

- Interac Online (Canada): In Canada, Interac Online is a popular payment method that allows customers to pay for online purchases directly from their bank accounts.

- SEPA (Single Euro Payments Area) Direct Debit: In Europe, SEPA Direct Debit enables customers to authorize direct debits for online purchases in euro currency across participating countries.

It’s important to note that the availability of these payment methods can vary based on the region, the e-tailer’s policies, and the banking infrastructure in place. Customers should check the payment options provided by the specific online retailer they are dealing with.

Advantages of bank transfers in e-tailing:

Here are some advantages of bank transfers in e-tailing:

- Security: Bank transfers are considered secure as they involve direct transactions between bank accounts. This can be reassuring for customers concerned about the safety of their financial information.

- Reduced Fraud: Compared to credit cards, bank transfers may have lower instances of fraud since they often require additional authentication steps.

- No Transaction Fees: Some customers prefer bank transfers because they may not involve additional transaction fees, which can be the case with credit card payments.

- No Chargebacks: Unlike credit card payments, which can be subject to chargebacks, bank transfers are generally irreversible once completed. This reduces the risk for the seller.

- Wider Accessibility: Bank transfers don’t rely on the availability of credit cards or specific digital wallets. Customers without credit cards can still make purchases using this method.

- Privacy: Bank transfers may offer more privacy compared to other payment methods, as they don’t necessarily require the sharing of credit card details or personal information with the seller.

However, it’s essential to consider that the main drawback is the time it takes for the funds to clear, making it less suitable for customers looking for instant transactions.

Disadvantages of Bank Transfers in Etailing :

Certainly, here are some disadvantages of bank transfers in e-tailing:

- Processing Time: Bank transfers typically take longer to process compared to instant payment methods. This delay can slow down order fulfillment and may not meet the expectations of customers looking for quick transactions.

- User Experience: The process of entering bank details and navigating through the payment steps can be perceived as less user-friendly compared to more streamlined payment options, potentially leading to cart abandonment.

- Error Prone: Bank transfers involve manual entry of account details, increasing the likelihood of errors. Mistakes in account numbers or other information can lead to payment issues and customer dissatisfaction.

- Lack of Chargeback Protection: Unlike credit card payments, bank transfers are often irrevocable. This means that if there is an issue with the transaction, such as receiving a defective product, customers may have limited recourse compared to chargebacks with credit cards.

- Limited Spontaneity: Given the processing time of bank transfers, they may not be suitable for impulse purchases or time-sensitive deals where customers expect immediate transaction confirmation.

- Dependency on Banking Infrastructure: The effectiveness of bank transfers relies on the efficiency of the banking infrastructure, and issues such as bank downtimes or technical glitches can impact the payment process.

It’s important for e-tailers to offer a variety of payment options to cater to different customer preferences and to balance the advantages and disadvantages associated with each method.

4. Buy Now Pay Later (BNPL) Services:

Offering the flexibility to make purchases and pay in instalments. Buy now, pay later (BNPL) services in e-tailing allow customers to make purchases and defer payment over time. Popular BNPL providers, like Afterpay, Klarna, and Affirm, offer a convenient payment option where users can split their total cost into smaller, interest-free installments. This can enhance the shopping experience and increase conversion rates for e-tailers while providing flexibility for consumers. However, it’s crucial for users to manage their payments responsibly to avoid late fees or interest charges.

“Buy Now, Pay Later” (BNPL) is a popular payment method in e-tailing that allows customers to make a purchase and pay for it in installments over time. Here are examples of BNPL services:

- Afterpay: Allows shoppers to buy products immediately and pay for them in four equal installments every two weeks. Afterpay is widely used in various online stores.

- Klarna: Offers flexible payment options, including the ability to pay later, pay in instalments, or pay immediately. Klarna is integrated into many e-commerce platforms.

- Affirm: Provides point-of-sale financing for online purchases, allowing customers to pay for their items over time with fixed monthly payments.

- Sezzle: Enables shoppers to split their total purchase into four interest-free installments, paid every two weeks.

- Quadpay: Allows customers to split their purchases into four payments over six weeks, with the first payment due at the time of the transaction.

- Zip (previously Quadpay): Offers interest-free installment payments, allowing customers to spread the cost of their purchase over time.

- Laybuy: Lets customers pay for their online purchases in six weekly payments, with no interest.

- PayPal Pay in 4: PayPal’s BNPL option, where customers can split their purchase into four equal payments every two weeks.

These BNPL services have gained popularity for providing flexibility to consumers while offering a straightforward and transparent payment process. However, users should be mindful of the terms and conditions associated with BNPL services to avoid potential fees or interest charges.

The advantages of Buy Now, Pay Later (BNPL) services include:

- Financial Flexibility: BNPL allows consumers to make purchases without paying the full amount upfront, providing financial flexibility and easing the burden of large expenses.

- Convenience: It enhances the shopping experience by streamlining the checkout process and offering a quick approval process, often without the need for traditional credit checks.

- Interest-Free Periods: Many BNPL services offer interest-free installment plans, making it an attractive option for those who want to spread payments without incurring additional costs.

- Increased Conversion Rates: E-tailers often experience higher conversion rates as BNPL options appeal to a broader audience, including those who might be deterred by the immediate full cost.

- Competitive Advantage: Offering BNPL can set businesses apart from competitors, attracting consumers who value flexibility in payment options.

- No Traditional Debt: Unlike traditional credit cards, BNPL plans typically don’t involve long-term debt, as each purchase is treated separately with a fixed payment schedule.

- Accessibility: BNPL services are often accessible to a wide range of consumers, including those with limited credit history or lower credit scores.

However, it’s crucial for users to use BNPL responsibly to avoid accumulating debt or facing late fees.

The disadvantages of Buy Now, Pay Later (BNPL) services include:

- Accumulation of Debt: Users may be tempted to overspend or accumulate debt if they regularly utilize BNPL services without careful budgeting.

- Late Fees and Interest Charges: Failure to make payments on time can result in late fees or interest charges, eroding the initial appeal of interest-free installment plans.

- Impact on Credit Scores: Some BNPL providers may report late payments to credit bureaus, potentially affecting users’ credit scores.

- Hidden Fees: Users should be aware of any hidden fees associated with BNPL services, such as transaction fees or fees for extending payment periods.

- Encourages Impulse Buying: The ease of BNPL transactions may lead to impulsive purchasing behavior, as consumers may not fully consider the long-term financial implications.

- Limited Merchant Acceptance: Not all merchants accept BNPL, restricting its availability for certain purchases.

- Dependency on Technology: As BNPL transactions heavily rely on digital platforms, technical issues or security concerns may disrupt the payment process.

- Potential for Over extension: While BNPL can provide short-term relief, users need to ensure they don’t overextend themselves financially by relying too heavily on deferred payments.

It’s important for consumers to carefully read terms and conditions, budget responsibly, and use BNPL services judiciously to avoid negative financial consequences.

5. Cryptocurrencies:

Some e-tailers accept cryptocurrencies like Bitcoin as a form of payment.

The advantages of incorporating cryptocurrencies into e-tailing payment processing include:

- Security: Cryptocurrencies use cryptographic techniques to secure transactions, reducing the risk of fraud and enhancing overall security compared to traditional payment methods.

- Reduced Transaction Costs: Cryptocurrency transactions often have lower processing fees compared to credit card transactions, leading to potential cost savings for e-tailers.

- Global Transactions: Cryptocurrencies facilitate seamless international transactions without the need for currency conversions or dealing with exchange rates, making cross-border e-commerce more efficient.

- Fast Transactions: Cryptocurrency transactions can be processed quickly, providing a faster payment experience for both merchants and customers, especially in comparison to traditional bank transfers.

- Financial Inclusion: Cryptocurrencies can provide financial access to individuals who are unbanked or underbanked, fostering inclusivity in the e-commerce landscape.

- Elimination of Chargebacks: Cryptocurrency transactions are irreversible, reducing the risk of chargebacks for merchants, which can be a common issue with traditional payment methods.

- Anonymity and Privacy: Cryptocurrencies offer a level of anonymity and privacy for users who value keeping their financial transactions discreet.

- Innovative Marketing Opportunities: Accepting cryptocurrencies can attract tech-savvy customers and position a business as forward-thinking, potentially offering a competitive advantage in the market.

While these advantages exist, it’s essential for businesses and consumers to consider factors such as regulatory compliance, volatility, and the evolving nature of the cryptocurrency landscape when integrating them into e-tailing payment processing.

The disadvantages of incorporating cryptocurrencies into e-tailing payment processing include:

- Volatility: Cryptocurrency prices can be highly volatile, posing a risk for both merchants and consumers. The value of a cryptocurrency can fluctuate significantly, leading to potential losses or gains.

- Limited Adoption: While cryptocurrency adoption is growing, it is not yet mainstream. Limited acceptance by merchants and consumers may restrict the usefulness of cryptocurrencies for e-tailers.

- Regulatory Uncertainty: Cryptocurrency regulations vary widely by jurisdiction, leading to uncertainty for businesses regarding compliance. Regulatory changes can impact the legality and use of cryptocurrencies in different regions.

- Security Concerns: While cryptocurrencies offer security benefits, the digital nature of transactions also introduces new security challenges, including the risk of hacking and other cyber threats.

- Lack of Consumer Understanding: Many consumers are still unfamiliar with cryptocurrencies, leading to hesitation or reluctance to use them for online purchases. Education is needed to increase awareness and confidence.

- Irreversibility of Transactions: While the irreversibility of transactions is an advantage for merchants, it can be a disadvantage for consumers who make errors or encounter issues with a purchase since refunds are challenging.

- Limited Consumer Protections: Cryptocurrency transactions typically lack the consumer protections provided by traditional payment methods, such as credit card chargebacks or fraud protection, making it riskier for buyers.

- Complexity of Implementation: Integrating cryptocurrency payment options can be complex for businesses, requiring additional technical infrastructure and resources.

Businesses considering cryptocurrency payment processing should carefully weigh these disadvantages against potential benefits and consider the specific characteristics of their target market and regulatory environment.

6. Mobile Payment Apps:

Mobile-specific apps like Venmo, Cash App, or Alipay that facilitate transactions through smartphones. In e-tailing payment processes, a mobile payment app facilitates convenient transactions. Users typically select items, proceed to checkout, and then choose the mobile payment option. The app securely processes the payment, often using methods like QR codes or NFC technology for quick and seamless transactions.

Examples of Mobile Payment Apps :

a) Apple Pay: Allows users to make secure payments using Apple devices. Apple Pay is a mobile payment and digital wallet service developed by Apple. It allows users to make payments using their Apple devices, such as iPhones, iPads, Apple Watches, and Macs.

Key features of Apple Pay include:

- Contactless Payments: Users can make secure, contactless payments at supported retailers by simply holding their Apple device near a contactless reader.

- In-App Purchases: Apple Pay can be used for quick and secure transactions within supported apps and online platforms.

- Apple Cash: Users can send and receive money through iMessage or use the Apple Cash card for payments.

- Security: Transactions are secured using Face ID, Touch ID, or device passcode. Actual card details are not stored on the device or Apple servers.

- Card Integration: Apple Pay supports credit and debit cards from various major banks and card issuers.

- Wallet App: The Wallet app on iOS devices stores digital versions of credit cards, loyalty cards, boarding passes, and more.

- International Use: Apple Pay is available in multiple countries and continues to expand its global reach.

Overall, Apple Pay provides a convenient and secure way for users to make payments both in-store and online, leveraging the capabilities of Apple’s hardware and software ecosystem.

b) Google Pay:

Google’s mobile payment solution for Android users. Google Pay is a mobile payment and digital wallet platform developed by Google.

Here are some key aspects of Google Pay:

- Contactless Payments: Users can make secure, contactless payments at supported retailers by tapping their Android devices near contactless terminals.

- In-App Purchases: Google Pay allows users to make quick and secure transactions within supported apps and online platforms.

- Card Integration: Users can add credit and debit cards to the Google Pay app, streamlining the payment process.

- Peer-to-Peer Payments: Google Pay enables users to send money to friends and family directly from the app.

- Google Pay Send: Formerly known as Google Wallet, this feature allows users to send money to others using their email address or phone number.

- Integration with Google Services: Google Pay is often integrated into various Google services, making it seamless for users to make payments within the Google ecosystem.

- Security: Google Pay uses multiple layers of security, including device authentication methods like fingerprint recognition or PIN, and tokenization to protect card information.

- International Use: Google Pay is available in multiple countries, allowing users to make payments and transactions globally.

Overall, Google Pay provides a convenient and versatile platform for users to make payments, both in-store and online, using their Android devices.

c) Samsung Pay:

Samsung Pay is a mobile payment and digital wallet service developed by Samsung Electronics.

Here are some key features of Samsung Pay:

- Magnetic Secure Transmission (MST): One distinctive feature of Samsung Pay is MST, which allows users to make payments at traditional magnetic stripe card terminals, in addition to NFC-enabled terminals. This enhances compatibility with a wide range of existing point-of-sale systems.

- NFC Technology: Like other mobile payment systems, Samsung Pay supports Near Field Communication (NFC) for contactless transactions at compatible terminals.

- Card Tokenization: Samsung Pay uses tokenization to secure transactions by replacing the actual card details with a unique token, enhancing security.

- In-App Purchases: Users can make secure transactions within supported apps and online platforms using Samsung Pay.

- Biometric Authentication: Samsung Pay supports biometric authentication methods such as fingerprint recognition and facial recognition for secure and convenient payments.

- Samsung Rewards: Users can earn points through the Samsung Rewards program by using Samsung Pay, which can be redeemed for various rewards.

- Membership and Loyalty Cards: Samsung Pay allows users to store and use membership cards, loyalty cards, and gift cards digitally.

- Samsung Pay Cash Card: Users can create a virtual prepaid card within Samsung Pay called Samsung Pay Cash, which can be used for payments.

Samsung Pay aims to provide users with a versatile and secure mobile payment experience, especially with its MST technology that sets it apart from some other mobile payment services.

d) Cash App:

Enables users to send and receive money and has a linked debit card for purchases. Cash App is a mobile payment service developed by Square, Inc.

Key features and aspects of Cash App:

- Peer-to-Peer Payments: Users can easily send and receive money to and from friends, family, or anyone with a Cash App account.

- Cash Card: Cash App provides users with a customizable debit card, known as the Cash Card, which is linked to their Cash App balance and can be used for making purchases online and in-store.

- Direct Deposit: Users can set up direct deposit to receive paychecks or other regular deposits directly into their Cash App account.

- Bitcoin Transactions: Cash App allows users to buy, sell, and transfer Bitcoin within the app.

- Cash Boost: Cash App offers a feature called Cash Boost, providing users with discounts or cashback rewards when they use their Cash Card at specific merchants.

- Investing: Users can invest in stocks and Bitcoin through Cash App.

- Cash App for Business: Cash App also offers features for small businesses, allowing them to accept payments and manage transactions.

- Security: Cash App includes security features such as Touch ID or Face ID for authentication, and transactions are encrypted.

Cash App is known for its simplicity and user-friendly interface, making it a popular choice for personal and small business transactions.

e) Venmo:

A mobile payment app that facilitates peer-to-peer transactions.Venmo is a mobile payment service owned by PayPal that facilitates peer-to-peer transactions.

Here are some key features of Venmo:

- Peer-to-Peer Transactions: Users can easily send and receive money to and from friends, family, or other Venmo users.

- Social Feed: Venmo includes a social feed that allows users to share and comment on transactions, adding a social element to the payment experience.

- Split Bills: Venmo makes it easy to split bills or expenses among a group of users, each contributing their share.

- Venmo Debit Card: Users can apply for and use a Venmo-branded debit card, which is linked to their Venmo balance, for making purchases.

- Bank Transfers: Venmo allows users to transfer funds between their Venmo account and their linked bank accounts.

- Payment Notes and Emojis: Users can add notes or emojis to their transactions, adding a personal touch to payments.

- Security Features: Venmo employs security measures such as encryption and account authentication to protect user information.

- Mobile App: Venmo is primarily accessed through its mobile app, available for both iOS and Android devices.

Venmo is popular among users for its social and interactive features, making it more than just a transactional tool—it’s also a social platform for sharing payments and experiences.

f) PayPal:

An online payment platform with a mobile app for various transactions. PayPal is a widely used online payment platform that enables users to make secure transactions over the internet.

Here are some key features of PayPal:

- Online Payments: Users can make purchases online by linking their credit or debit cards, or by using funds available in their PayPal account.

- Peer-to-Peer Transactions: PayPal allows users to send and receive money to and from friends, family, or anyone with a PayPal account.

- International Transactions: PayPal facilitates cross-border transactions and currency conversions, making it useful for international payments.

- PayPal.me: Users can create a personalized PayPal.me link, making it easy for others to send them money.

- PayPal Debit Card: Users can apply for a PayPal-branded debit card, linked to their PayPal balance, for making purchases and ATM withdrawals.

- Business Solutions: PayPal offers solutions for businesses, including payment processing, invoicing, and e-commerce integration.

- One Touch: Users can enable One Touch to stay logged in on their devices, streamlining the checkout process for subsequent transactions.

- Security Measures: PayPal employs encryption and fraud prevention tools to enhance the security of transactions and user accounts.

PayPal is widely accepted by online merchants and is used by individuals and businesses alike for its convenience and security in processing digital transactions.

g) Zelle:

A digital payments network often integrated into banking apps for peer-to-peer transfers. Zelle is a peer-to-peer payment service that allows users to send and receive money quickly and securely through participating banks and credit unions.

Key features of Zelle include:

- Bank Integration: Zelle is often integrated into the mobile banking apps of participating financial institutions, allowing users to send money directly from their bank accounts.

- Real-Time Transactions: Zelle provides real-time money transfers between users, making it a fast and convenient option for peer-to-peer transactions.

- Email or Phone Number Transactions: Users can send money to others using their email address or phone number associated with their bank account.

- Splitting Bills: Zelle allows users to split bills or expenses with others, dividing the cost among multiple recipients.

- No Fee for Standard Transactions: In many cases, Zelle transactions are free, although users should check with their specific bank for any applicable fees.

- Security Measures: Zelle employs security measures to protect transactions, and users should only transact with people they know and trust.

- Mobile App: Zelle also has a standalone mobile app that users can use to send and receive money.

It’s important to note that Zelle’s availability may vary based on the user’s banking relationship, as not all banks or credit unions offer Zelle integration.

h) Square Cash (Cash App):

Developed by Square, it allows users to send money and make purchases. Square Cash, now officially known as Cash App, is a mobile payment service developed by Square, Inc.

Here are some key features and aspects of Cash App:

- Peer-to-Peer Transactions: Users can easily send and receive money to and from friends, family, or other Cash App users.

- Cash Card: Cash App provides users with a customizable debit card, known as the Cash Card, which is linked to their Cash App balance and can be used for making purchases online and in-store.

- Direct Deposit: Users can set up direct deposit to receive paychecks or other regular deposits directly into their Cash App account.

- Bitcoin Transactions: Cash App allows users to buy, sell, and transfer Bitcoin within the app.

- Cash Boost: Cash App offers a feature called Cash Boost, providing users with discounts or cashback rewards when they use their Cash Card at specific merchants.

- Investing: Users can invest in stocks and Bitcoin through Cash App.

- Cash App for Business: Cash App also offers features for small businesses, allowing them to accept payments and manage transactions.

- Security: Cash App includes security features such as Touch ID or Face ID for authentication, and transactions are encrypted.

Cash App is known for its simplicity and user-friendly interface, making it a popular choice for personal and small business transactions. Please note that the app’s features may evolve, so it’s advisable to check the latest information from the official source or within the app itself.

i) Facebook Pay:

A feature within Facebook apps for sending money to friends and making purchases. Facebook Pay is a payment service offered by Facebook, Inc. It is designed to provide a convenient and secure way for users to make payments on various Facebook-owned platforms.

Here are some key features of Facebook Pay:

- Cross-Platform Integration: Facebook Pay is integrated across various Facebook-owned apps and services, including Facebook, Messenger, Instagram, and WhatsApp.

- Peer-to-Peer Payments: Users can send money to friends and family within the Facebook ecosystem.

- In-App Purchases: Facebook Pay can be used to make purchases within supported apps and games on the Facebook platform.

- Charitable Donations: Users can contribute to fundraisers and make donations to supported causes through Facebook Pay.

- Security Features: Facebook Pay includes security measures such as PIN protection and the ability to use biometric authentication methods like fingerprint recognition or facial recognition.

- Payment History: Users can view their payment history and manage payment methods within the Facebook Pay settings.

- International Payments: Facebook Pay supports payments in different currencies and is available in multiple countries.

It’s important to note that Facebook Pay is distinct from the cryptocurrency Libra, which was initially proposed by Facebook but has undergone changes and is now known as Diem. Users can set up Facebook Pay within the settings of the individual apps and link their preferred payment method for transactions.

j) Paytm:

A popular mobile payment app in India, offering a range of financial services. Paytm is a popular digital payment platform based in India.

Here are some key features and aspects of Paytm:

- Mobile Wallet: Paytm started as a mobile wallet, allowing users to store money in the app and use it for various transactions.

- Peer-to-Peer Transactions: Users can send money to friends, family, or anyone with a Paytm account.

- Mobile Recharge and Bill Payments: Paytm enables users to recharge their mobile phones, pay utility bills, and recharge DTH services.

- Online and In-Store Payments: Users can make payments at online and offline merchants, both online and in physical stores, using the Paytm app.

- QR Code Payments: Paytm uses QR codes for transactions, allowing users to scan merchant QR codes or share their own for quick payments.

- Ticket Booking: Paytm provides services for booking flights, trains, buses, and movie tickets.

- Shopping: Paytm has an integrated e-commerce platform where users can buy a wide range of products.

- Investment and Banking Services: Paytm offers features like Paytm Money for mutual fund investments and Paytm Payments Bank for banking services.

- Insurance: Users can purchase insurance products through the Paytm app.

- Cashback and Offers: Paytm often provides cashback offer and discounts for various transactions.

Paytm has become a comprehensive financial services platform, offering a variety of services beyond basic digital payments. It has gained widespread popularity in India and continues to expand its range of offerings.

These apps make it convenient for users to handle transactions, whether it’s splitting bills, making purchases, or transferring money to friends and family.

Advantages of Mobile Payment Apps :

- Convenience: Mobile payment apps offer a convenient way for users to make purchases anytime, anywhere, using their smartphones.

- Speed and Efficiency: Transactions through mobile payment apps are generally faster than traditional methods, reducing checkout time and improving the overall shopping experience.

- Security: Many mobile payment apps use encryption and secure authentication methods, enhancing the security of financial transactions and protecting user data.

- Integration with Loyalty Programs: Some mobile payment apps integrate with loyalty programs, offering users rewards, discounts, or cashback incentives for using the app for purchases.

- Reduced Need for Physical Cards: Users can store multiple payment methods within the app, reducing the need to carry physical credit or debit cards.

- Access to Digital Receipts: Mobile payment apps often provide digital receipts, helping users keep track of their transactions and facilitating easier returns or exchanges.

- In-app Offers and Promotions: E-tailers can use mobile payment apps to push targeted offers and promotions, enhancing the shopping experience and encouraging customer loyalty.

- Compatibility with Various Devices: Mobile payment apps are designed to work across different devices, ensuring a broad user base and accessibility for customers with various smartphones.

- Contactless Transactions: With features like NFC, mobile payment apps enable contactless transactions, promoting hygiene and safety, especially in situations like the COVID-19 pandemic.

- User-Friendly Interfaces: Mobile payment apps often have user-friendly interfaces, making it easy for customers to navigate, manage payment methods, and complete transactions effortlessly.

Disadvantages of Mobile Payment App :

- Technical Issues: Mobile payment apps may experience technical glitches, such as server downtimes or connectivity issues, leading to potential disruptions in the payment process.

- Security Concerns: Despite advancements in security measures, mobile payment apps are susceptible to hacking, fraud, or unauthorized access, posing a risk to users’ financial information.

- Dependency on Technology: Users relying solely on mobile payment apps may face challenges if their device battery dies, if there’s no network coverage, or if the app malfunctions, hindering their ability to make payments.

- Limited Acceptance: Not all retailers or e-tailers accept every mobile payment app, leading to inconvenience for users who may need to use multiple apps depending on where they shop.

- Privacy Issues: Mobile payment apps often collect user data for various purposes, raising concerns about privacy and how that information is used or shared by app providers.

- Compatibility Issues: Some mobile payment apps may not be compatible with older smartphones or certain operating systems, limiting access for users with outdated devices.

- Fraudulent Activities: As mobile payment usage increases, so does the risk of fraudulent activities, including phishing scams, fake apps, or identity theft targeting unsuspecting users.

- Transaction Limits: Some mobile payment apps impose transaction limits, which can be restrictive for users making large purchases or frequent transactions.

- Dependency on Internet Connectivity: Mobile payment apps heavily rely on internet connectivity. Poor or unstable internet connections can lead to transaction failures or delays.

- Learning Curve: Older or less tech-savvy individuals may find it challenging to adapt to using mobile payment apps, creating a potential barrier for certain demographics.

7. Cash on Delivery

Cash on Delivery (COD) is a payment option in e-tailing where customers pay for their purchases in cash at the time of delivery.

Here are some aspects related to Cash on Delivery in e-tailing payment processing:

- Customer Trust: COD can build trust as customers pay only when they receive the product, ensuring it meets their expectations, especially in regions where online transactions may be viewed with skepticism.

- Accessibility: COD caters to customers who may not have access to digital payment methods or prefer not to share financial information online.

- Reduced Cart Abandonment: Offering COD can reduce cart abandonment rates, as some customers might be hesitant to complete a purchase if only online payment options are available.

- Market Penetration in Cash-Driven Economies: In regions where cash transactions are prevalent, COD facilitates market penetration for e-tailers by accommodating local payment preferences.

- No Online Transaction Risks: Customers avoid the risks associated with online transactions, such as fraud or unauthorized charges, as they pay in cash upon receiving the product.

Challenges and considerations of Cash on Delivery:

- Operational Costs: COD involves additional operational costs for logistics and payment collection at the time of delivery.

- Payments: E-tailers face delays in receiving payments since they occur only upon product delivery, potentially affecting cash flow.

- Risk of Non-Payment: There’s a risk of customers refusing to pay upon delivery, leading to additional logistics costs and potential losses for the e-tailer.

- Limited Tracking: COD transactions may lack the tracking and confirmation associated with digital payment methods, making it harder to manage and track orders.

- Limited Reach: In the age of digital transactions, COD may limit the e-tailer’s reach to a certain demographic, excluding those who prefer or are accustomed to digital payments.

Ultimately, the decision to offer COD depends on the target market, customer preferences, and the e-tailer’s ability to manage associated challenges.

Cash on Delivery (COD) in e-tailing payment processing offers several advantages:

- Customer Convenience: COD provides customers with the convenience of paying in cash upon receiving the product, eliminating the need for online transactions or pre-payment.

- Increased Trust: COD builds trust, especially in regions where online transactions may be viewed with skepticism. Customers feel more secure paying only when they physically receive the ordered items.

- Accessible to All Customers: COD caters to customers who may not have access to digital payment methods or credit cards, broadening the customer base for e-tailers.

- Reduced Cart Abandonment: Offering COD can reduce cart abandonment rates, as some customers may be hesitant to proceed with a purchase if only online payment options are available.

- Market Penetration: In regions where cash transactions are predominant, COD facilitates market penetration for e-tailers by aligning with local payment preferences.

- No Online Transaction Risks: Customers avoid online transaction risks such as fraud or unauthorized charges since payment occurs in cash upon delivery.

- Flexibility for Buyers: COD provides flexibility for buyers who may want to inspect the product before making a payment, ensuring it meets their expectations.

- Overcoming Digital Literacy Barriers: In areas with low digital literacy, COD helps overcome barriers associated with using digital payment methods, making online shopping more accessible.

- Immediate Payment Confirmation: E-tailers receive immediate confirmation of payment upon delivery, ensuring timely verification of successful transactions.

- Adaptation to Local Customs: Offering COD shows an understanding and adaptation to local customs and preferences, enhancing the appeal of an e-tailer in diverse markets.

While COD has these advantages, it’s essential for e-tailers to carefully consider the associated operational costs, potential delays in payments, and the risk of non-payment. Balancing payment options to cater to diverse customer preferences is crucial for a successful e-tailing strategy.

Disadvantages of Cash on Delivery (COD) in e-tailing payment:

- Operational Costs: E-tailers incur additional operational costs associated with handling cash payments during delivery, including logistics, security, and administrative expenses.

- Delayed Payments: COD transactions result in delayed payments for e-tailers since they receive funds only upon product delivery. This can impact cash flow and financial planning.

- Risk of Non-Payment: There is a risk of customers refusing to pay or providing insufficient funds upon delivery, leading to losses for the e-tailer.

- Logistical Challenges: Managing cash transactions during delivery poses logistical challenges, including the need for secure cash handling and reconciliation processes.

- Limited Tracking and Confirmation: COD transactions may lack the tracking and confirmation mechanisms associated with digital payments, making it challenging for e-tailers to monitor and manage orders effectively.

- Potential for Fraud: The cash handling process during COD transactions can be susceptible to fraud, both from customers and delivery personnel.

- Impact on Customer Experience: Some customers may find the need to have cash on hand inconvenient, potentially impacting their overall shopping experience.

- Reduced Efficiency: COD can slow down the order fulfillment process, especially if customers are not prepared with the exact cash amount or if there are delays in counting and verifying payment.

- Limited Customer Insights: E-tailers may miss out on valuable customer data and insights associated with digital transactions, limiting their ability to understand and cater to customer preferences.

- Exclusion of Digital-Only Shoppers: Offering only COD as a payment option may exclude customers who prefer or are accustomed to digital payment methods, limiting the e-tailer’s reach.

Balancing the benefits and drawbacks, e-tailers often need to carefully assess their target market, customer preferences, and the overall impact on their business operations when deciding whether to offer COD as a payment option.

Challenges:

People in India (in small towns and villages) the small runover villages are not accustomed to online shopping system. The online payment system through the credit card is also totally alien to them. Most of them do not avail of the transaction facilities offered by the credit cards. Both technological and legal tools should be used to enhance the security of e-Tailing.

Payment Preferences in India is predominantly a cash economy. Despite government-led initiatives such as Digital India, Jan Dhan Yojana-Aadhaar-Mobile (JAM) scheme, and demonetization, which were in part geared to encourage a less-cash economy, much of India continues to prefer dealing in cash. Further, while Delhi, Mumbai, Bangalore, Hyderabad, and Kolkata have shown an increase in digital payments, lower tier cities are yet to shift their payment preferences. Overall, 60% of the total e-Tailing payments in India are still made using the cash-on-delivery (COD) option. Even as the reluctance to go cashless remains, India’s digital payments infrastructure is evolving to address the security, convenience, and accessibility concerns of Indian users. This is evident in the proliferation of startups in India’s financial technology sector. More than 600 new enterprises have emerged in the field of lending, payments, insurance, and trading.

Conclusion: –

In conclusion, diverse payment options in e-tailing enhance customer convenience, fostering a positive shopping experience. Offering various methods such as credit cards, digital wallets, and buy-now-pay-later services caters to different preferences, boosting sales and customer satisfaction. The success of e-tailing hinges on the strategic implementation of versatile payment options. A varied selection, including credit cards, digital wallets, and other emerging methods, ensures broader customer accessibility, fosters trust, and plays a pivotal role in the overall growth and competitiveness of online retail businesses.

To sum up, a well-rounded selection of payment options in e-tailing is crucial for accommodating diverse customer preferences. This not only improves the overall shopping experience but also contributes to increased trust, convenience, and ultimately, higher conversion rates for online retailers.